Gain deep knowledge of cashflow, productivity, liquidity, and stability through practical, advanced business management techniques designed for today’s professionals.

Master Core Business Management Skills

Business

Management

Made Practical

This tailored content empowers entrepreneurs, educators, and consultants with cutting-edge resources on economic fundamentals and business strategy, focusing on actionable results and sustainable growth.

40

Years of Experience in Business Management Teaching and Consulting. Programmer in Excel.

Business-Management.Basics- for-Entrepreneurs- Analysts-Planners

A PDF with 80 pages.

Not a perfect textbook, but there are a few special features.

Link for download:

Domain :

www.business-

management-for-entrepreneurs.com

Last actualisation 2026 04 07

Comprehensive Basics

Foundational concepts like cashflow and liquidity explained with clarity and depth.

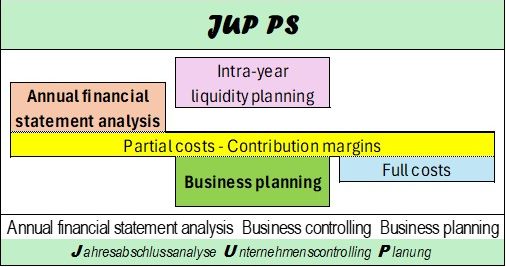

Left: Scheme of the most popular Excel-based program JUP PS of the author (for German agriculture).

The same terms in partial costs analysis (past) as in business planning (future) - barrier-free.

Targeted for Entrepreneurs

Customized resources designed to support effective decision-making and planning.

Even those who drop out of their degree course or those which studying business management as a minor subject need to learn concepts like profitability, liquidity and stability.

At any rate, these terms must be focused right from the start.

Educational Focus

Valuable knowledge crafted for teachers and academic professionals.

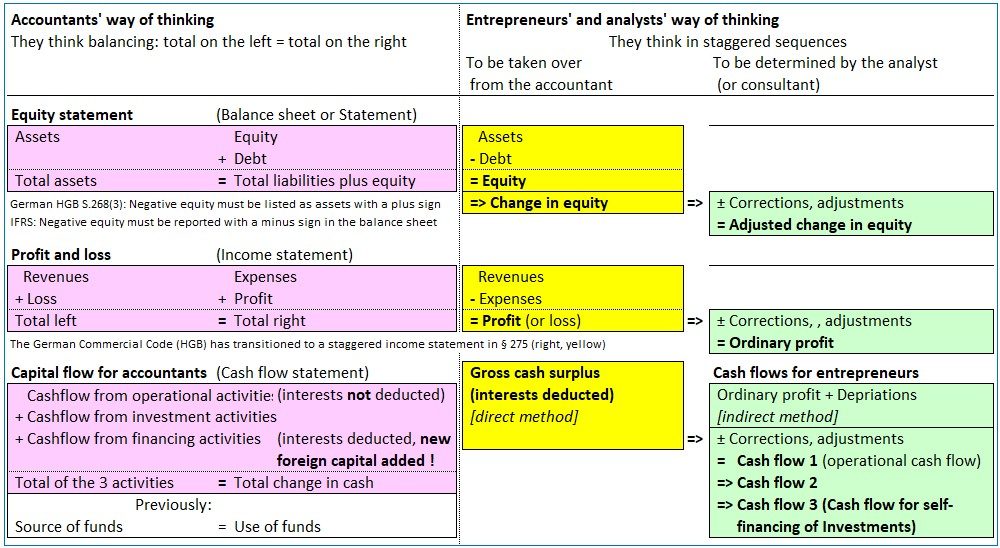

Beginners, in particular, do not need to be trained to think like accountants; rather, they need to learn how to run a business.

The accountant's "standards" like IFRS 18 are far away from that, what any entrepreneur, any company and any student needs !

Look for terms that can help in business management

Innovative tools and insights to enhance business advisory services.

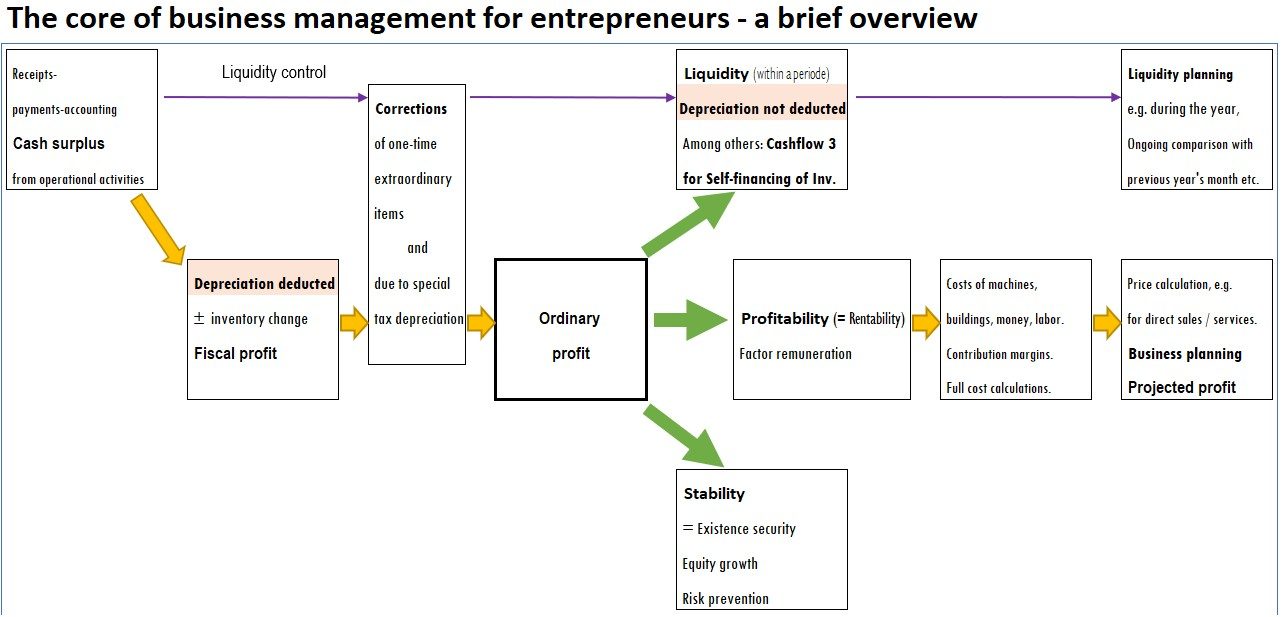

There are various types of cash flow, such as ‘free cash flow’. This term shall show how much ist left for stockholders.

However, the important cash flow for an entrepreneur is ‘cash flow for self-financing of investments’ (= Cash flow 3).

Business Management - Basics for Entrepreneurs Analysts Planners

Contents of the whole edition - PDF

1. The Core of Business Management

2. Important pairs of terms: income and expenses, etc.

3. Business annual financial statements - derived from the annual financial statements in accordance to fiscal and commersial laws

3.1 Profit and Loss Statement (P&L)

3.1.1 Profit

3.1.2 Ordinary profit

3.1.3 EBIT and EBITDA

3.2 Balance sheet

3.2.1 Assets within the company

3.2.2 Borrowed capital

3.2.3 Equity

3.2.4 Depts not covered by assets

3.2.5 Extraordinary items on the liabilities side

3.3 Indispensable supplements for analysis

3.3.1 Capacities and production processes

3.3.2 List of individual loans and short-term liabilities

3.4 Additional reports from the accounting office

4. Profitability, liquidity and stability – the first step of assessement

4.1 Profitability

4.1.1 Share of fixed costs in total contribution margin %

4.1.2 Profit rate %

4.1.3 Profitability of all factors combined

Relative factor remuneration %

Net profitability %

4.1.4 Profitability of individual factors labor, land and capital

Earnings from labor per hour

Ground rent per hectar

Total return on capital %

4.2 Liquidity – including deposits and withdrawals

4.2.1 About the term ‘cash flow’ – a preliminary check

4.2.2 Gross cash surplus

4.2.3 The two methods for deriving cash flows

4.2.4 The three most important cash flows for entrepreneurs

Cash flow 1 = operational cash flow

Cash flow 2 = cash flow for repayments and self-financing of investments

Cash flow 3 = cash flow for self-financing of investments

4.2.5 Adjusted deposits and adjusted withdrawals

4.2.6 Repayments according to business management principles

4.2.7 Benchmarks for cash flows

Depreciation (= replacement investments),

Long-term and mid-term benchmarks

Replacement investment coverage rate %

4.2.8 Debt service limits and their utilisation %

4.2.9 Advantages of cash flow for self-financing of investments

4.3 Stability

4.3.1 Adjusted change in equity

4.3.2 Equity ratio %

4.3.3 Debt coverage %

4.3.4 Degree of obsolescence %

4.4 Income statement and cash flow statement according to IFRS 18

5. Costs-benefits-calculation – the second step of assessement

5.1 Controlling in business management

5.2 Partial costs

5.2.1 Benefits, variable costs and contribution margins

5.2.2 Total contribution margin

5.2.3 Fixed costs and overhead costs

5.2.4 Ancillary benefits

5.2.5 Share of fixed costs on the total contribution margin %

5.3 Full costs

5.3.1 Full cost breakdown according to German Agricultural Society (DLG)

5.3.2 Contribution margin calculation embedded in full costs scheme

5.4 Unit costs

5.5 Costs calculation with company allocation sheet

5.5.1 From P&L scheme to contribution margin scheme

5.5.2 Full costs calculation based on company allocation sheet

5.6 Costs calculation without company allocation sheet

5.6.1 From contribution margin scheme to P&L scheme

5.6.2 Full costs calculation based on contribution margins

5.7 Embedding of special analysis – the example of viticulture

6. Consolidated financial statement of several sub-operations

7. Intra-year liquidity planning

8. Mid-term operational planning

8.1 Sensitivity

8.2 Amortisation

8.3 Planning with contribution margin versus without contribution margin

8.4 Static versus dynamic planning

8.5 Actual year – which one?

Current actual

Calculated actual

Optimized actual

Accounting actual

8.6 Alternative target companies

8.7 Year-on-year planning

8.8 Forecast of short-term liabilities

8.9 Actual/plan versus plan/actual

9. Double-entry bookkeeping

9.1 Double-entry bookkeeping with plus and minus

9.2 Double-entry bookkeeping with debits and credits